Having access to liquidity has been a major issue for humankind for financing both personal life aspects (e.g., housing, cars, college) and for business initiatives (e.g., starting, growing, and expanding a business). The amount of uncertainty that both faces of this exchange – i.e., the creditor and the prospective debtor – face are paramount. On the one hand, the creditor tries to fill in all blanks about the prospect’s capacity to pay the loan requesting additional information, information that in some cases is difficult to obtain by the debtor, resulting in lost opportunities for both sides. On the other hand, the prospect faces a black box interaction, with an approval process that happens behind doors and whose criteria aren’t clear, so the prospective debtor cannot work on adjusting her score.

Artificial Intelligence has played a major role in solving the first side of the equation -the creditor side-, bringing an objective and reproducible credit score estimation of the prospective debtor, at the expense of bringing further opacity to the process for the prospective debtor. In this blog post, we will go through the current paradigm and how we could tackle it differently to perform a more comprehensive approach, identifying current limitations as well as potential solutions from an AI point of view. The ideas described in this article can be applied to both financial entities and subscription-based business models that face default as a source of involuntary churn.

Traditional credit scoring uses blackbox methods -either a human that is out of reach from the end-client or a statistical model- which weights various factors including demographic factors, payment history and other financial indicators. This traditional approach will deny credit to consumers without considering the possibility to adjust their current situation or other extenuating factors. In this sense, it’s modeled as the likelihood at the time of approval of a prospective debtor to pay in full or default. We observe two main limitations:

One-side interaction: the interaction tends to be one-sided with small room for negotiation. Debtors and creditors should be able to update their terms & conditions to maximize the chance of a mutually beneficial interaction. A hard rejection will move the client to a different institution, being a fully-wasted opportunity for the creditor that could be -in some cases- easily transformed into an approval to a different kind of deal.

One-shot decision: assuming the decision and conditions are a one-shot process. We should consider credit scoring strategies that continuously re-assess the default probability and adjust new conditions accordingly.

So, our view on Artificial Intelligence applied to credit scoring is a dynamic interaction, where the model suggests and re-assesses conditions to maximize the mutual benefits on a continuous basis.

Modeling and data

So, we can formalize a credit scoring model as a function that, given the prospective debtor, the creditor conditions and the request loan characteristics predicts a valuable KPI for decision making such as the default probability, the expected ROI, etc.

Just for illustrative purposes, such information may comprise:

Debtor:

Demographic: age, profession, education, etc.

Financial records: income and spending, debts, mortgages, etc.

Creditor: portfolio, cash flow, market indicators, etc.

Loan conditions: the amount of money loaned, spread, annual percentage rate, timeline, guarantors, consequences in case of contract breach, etc.

We can use any model to encode the aforementioned function (e.g., scorecards, decision trees, neural networks).

As mentioned in the previous section, our view on credit scoring considers not just the end decision (i.e., approval vs. rejection) but the adjustment of the loan conditions to ensure a mutually beneficial outcome. So, an AI model should use the aforementioned function to discover the conditions that maximize your KPI

So, we can transform a rejection to an initial submission into approval of an alternative. Please note that while we are simplifying the search for the loan condition adjustment, the model could as well suggest changes to the debtor information. For instance, it could suggest that the easier way of approving the credit is to increase the debtor’s salary by a certain amount, or by reduce his monthly expenses. We prioritize changes on load conditions because they can be applied instantly while looking for approval through the client’s adjustment tend to require longer feedback loops.

However, regardless of our KPI or modeling strategy, we need to be careful about corner cases such as predicting that by lowering the interest rate to zero the chance of a client paying will maximize, leading to a zero profit for the creditor. Similarly, increasing the interest to infinity to maximize profit, but in practice, leads to prospects turning down the loan or getting into bankruptcy. If you’re facing this issue, take a look at causal modeling and monotonic models or simply embed some domain-driven constraints in the decision process.

Course, Templates

Data Ignite

Create bulletproof AI solutions following our methodology.

When dealing with credits, the ability to explain why a certain loan was not conceived, as well as the conditions that were not met, plays a central role. It is not only relevant for those in the receiving end, but also for those who could profit from the deal, if it had happened.

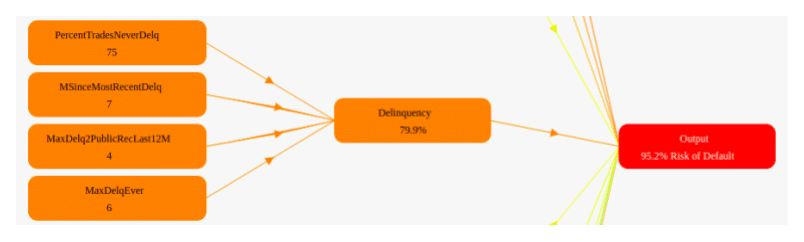

When one models the problem by changing the conditions and context of a client one can infer counterfactual explanations and come up with a hypothesis on how the client could be accepted, and what needs to be changed versus the reality.

Various models have been developed to conceptualize reasons and explanations on the decisions made, an interesting example of this is the model made by Cynthia Rudin’s team for the FICO Data Challenge. The strategy groups features by subscales and attributes to each of these subscales a miniature model (with a softmax). These miniature models are non-linear and thus, by doing so, one can build a tree-like model with machine learning under the hood. A demo of their work can be seen here.

Despite all advantages that machine learning models carry, they are also associated with biases. It may be the data you’re using is already biased, the historical decisions made by humans are biased, or the sampling chosen is not representative, or you may be using the wrong algorithm or KPI for the specific problem. The fact is that there will always be some type of bias, and in credit scoring, we have to guarantee that our models are not tending to a specific race, or gender, for example. Note that biased decisions aren’t only prejudicial for the end customer but also for the financial institution. Having models that rely on spurious correlations will eventually lead to catastrophic failure.

Tools like Aequitas, AI Fairness 360, and What-If are open-source toolkits that data scientists can use to check for bias ad discrimination in machine learning models. These tools allow for informed and equitable decisions around developing and deploying predictive tools. More on these tools here.

If you want to learn more about Fairness in AI, check our previous post.

Conclusion

A change in the actual paradigm of credit attribution could benefit both parties. More deals could be made, and, more importantly, more deals can be completely fulfilled as time goes by. We live in a fast-paced world, surrounded by continuous changes and new opportunities, why would we oversimplify and assume static solutions to dynamic environments?

Master customer retention rate calculation with this practical guide. Learn the formulas, see real-world examples, and get actionable tips for business growth.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.